Bitcoin’s protocol still runs almost unchanged from the rules Satoshi Nakamoto wrote down in 2008. But the user experience, the economic structure, and the governance reality of the system have drifted considerably from the early design picture. Reading the whitepaper or the visual glossary gives a faithful picture of the protocol but a misleading picture of what most users actually touch. This entry walks through four axes where the gap is largest, with pointers to the records.

| Axis | Early design picture | Current reality | Drift started |

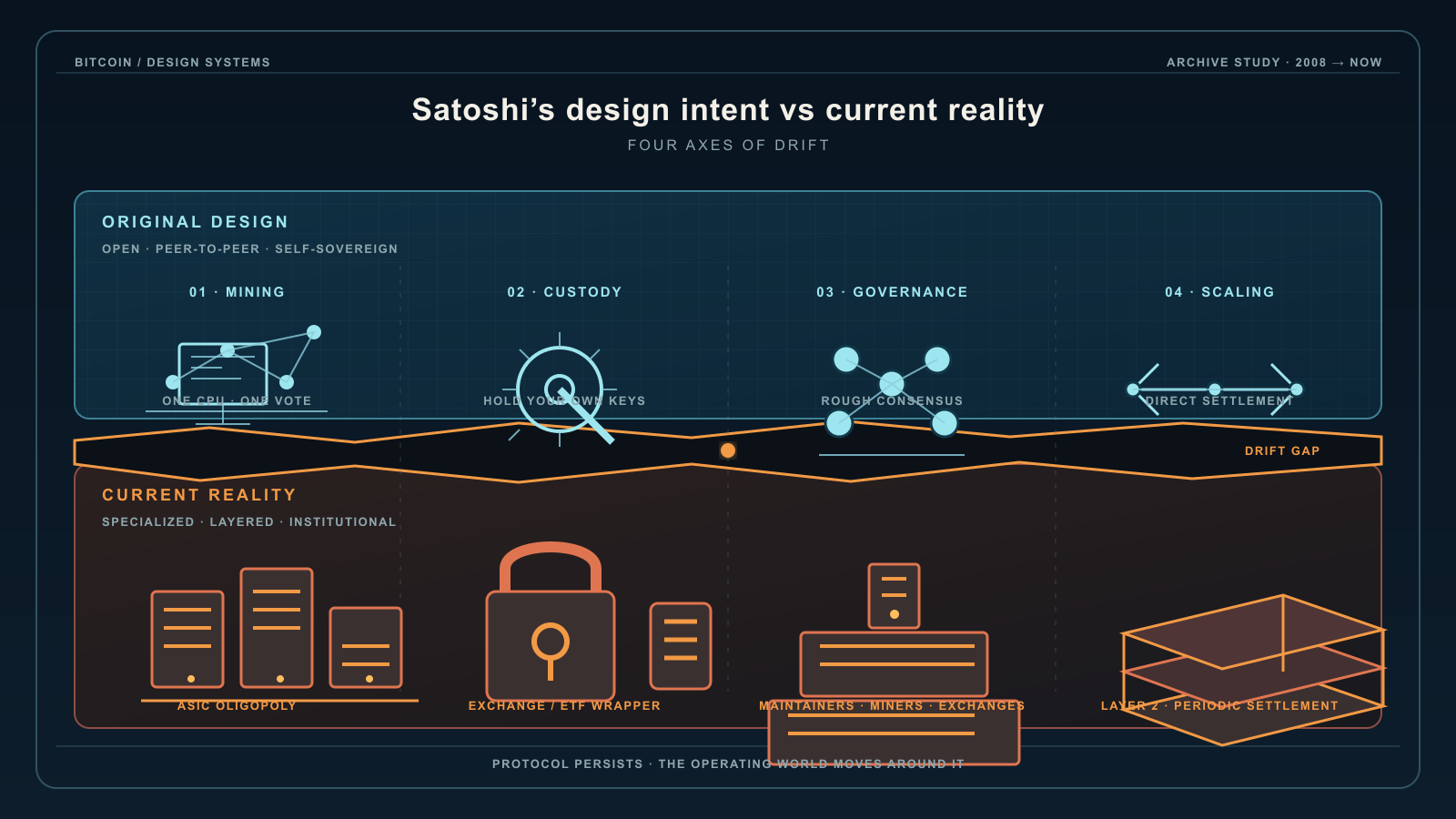

|---|---|---|---|

| Mining | ”one-CPU-one-vote” | ASIC oligopoly | 2010 GPU, 2013 ASIC |

| Custody | Each user holds private keys | Exchange IOUs / ETF wrappers | 2011 onwards (Mt. Gox) |

| Governance | Rough consensus among nodes | Bitcoin Core maintainers + large miners | Dec 2010 (Satoshi → Gavin handover) |

| Scaling | Direct P2P transactions | Layer-2 (SegWit/Lightning) + custodial off-chain | 2010 1 MB cap, 2017 SegWit |

1. Mining — “one-CPU-one-vote” → ASIC oligopoly

Satoshi wrote (whitepaper § 4, “Proof-of-Work”): “Proof-of-work is essentially one-CPU-one-vote.” The implicit assumption was that mining would stay on general-purpose computers — anyone with a PC could participate, and the network’s defence rested on a wide population of ordinary nodes also producing blocks.

The reality. Mining moved off PCs onto purpose-built chips called ASICs in 2013. Bitcoin’s first commercial ASIC was the Avalon ASIC (January 2013); Bitmain, founded later that year, became the dominant manufacturer through the 2015 – 2018 era. A modern ASIC computes Bitcoin’s hash function tens of millions of times faster per kilowatt-hour than any general-purpose computer, which means a PC running against ASIC competition burns electricity and produces nothing. Mining today is a heavy-industrial activity concentrated in a handful of pools and a handful of geographies, not a participatory side-activity of running a node.

When the drift started. GPU mining started in May 2010 (Laszlo Hanyecz, the same developer who later paid 10,000 BTC for pizza). Satoshi expressed unease at the time, asking Hanyecz to slow down — see Hanyecz’s account of the exchange for the recorded conversation. FPGA mining followed in 2011, and ASIC mining in 2013. Satoshi disappeared in April 2011, so the entire ASIC era is post-Satoshi. The chronology is documented; the reason for the departure is not (no surviving Satoshi statement ties leaving to the mining-hardware drift specifically).

The centralisation consequence. Worked through in Ray Dillinger’s 2018 interview and in the mining-reward exhaustion analysis.

2. Custody — own your keys → exchange IOUs (and ETF wrappers)

Satoshi wrote (whitepaper § 1, “Introduction”): “What is needed is an electronic payment system based on cryptographic proof instead of trust, allowing any two willing parties to transact directly with each other without the need for a trusted third party.” The design assumes each user holds their own private keys — that is the only way you can sign transactions yourself.

The reality. A large share of people who “own bitcoin” today — particularly those who acquired it through an exchange or an ETF — do not hold any keys. They have an account balance at an exchange (Coinbase, Binance, Kraken, etc.) or a share in a fund, which puts a “trusted third party” exactly where the whitepaper opens by ruling one out. Functionally these are bitcoin-denominated IOUs from custodial businesses, indistinguishable from a brokerage account. The community shorthand for this is “not your keys, not your coins.”

The institutional limit: spot ETFs. The trend went further in January 2024 when the US SEC approved the first spot Bitcoin ETFs (BlackRock IBIT, Fidelity FBTC, etc.). ETF shareholders hold no bitcoin at all — only equity in a fund whose custodian holds bitcoin on their behalf. Within months these ETFs collectively held several hundred thousand BTC. This is the custody axis taken to its institutional limit: the “peer-to-peer electronic cash” of the whitepaper has, for most retail and institutional money, become a traditional asset class accessed through brokerage plumbing.

Why it matters. When the custodian fails, the IOU does not pay out. The Mt. Gox bankruptcy in February 2014 lost roughly 850,000 BTC of customer holdings; the FTX collapse in November 2022 repeated the pattern with a different generation of operators. In each case the affected users had no protocol-level claim on any coin — they had a contractual claim against an insolvent company. This is the bank-failure mode Bitcoin was designed to make impossible at the protocol level, recreated above the protocol by user choice and product design. Both collapses are catalogued in more detail — alongside the other iconic Bitcoin loss cases, grouped by loss mechanism — in Lost Bitcoin: Thomas, Howells, QuadrigaCX, Mt. Gox, FTX and the irreversibility lesson.

3. Governance — distributed consensus → core developers + large miners

Satoshi wrote (whitepaper § 5, “Network”): “They [nodes] vote with their CPU power, expressing their acceptance of valid blocks by working on extending them…” The picture is of consensus emerging mechanically from the work of many independent operators, with no privileged decision-maker.

The reality. Protocol changes today are gated by a layered web of actors: the Bitcoin Core software’s maintainer team (a small group of contributors with commit access) sets what the canonical client can do; large mining pools, major exchanges, custodians, and economic node operators each carry an effective veto by deciding what software to run; ordinary node operators participate by choosing which version to install. The 2017 UASF episode showed that a coordinated user push can override miner preferences in principle, but the practical decision-making concentrates among the small number of actors with operational weight. The diagram below simplifies this to two layers for readability — in practice the influence relationships run between more parties than shown.

When the drift started. Three inflection points:

- December 2010: Satoshi handed maintenance authority to Gavin Andresen, without consulting Gavin first. Gavin in turn added four other developers to the commit list — chosen for being present and helpful rather than through any formal process. That is the seed of the modern Core maintainer team.

- 2015 – 2017: The block size war. See Bitcoin Fork Wars as Not OSS. The conflict was decided through a combination of SegWit activation (BIP 141), the user-activated soft fork (UASF) pressure, the failure of the New York Agreement, and the Bitcoin Cash split — a multi-front political/economic process rather than the rough consensus the whitepaper describes.

- January 2016: Mike Hearn declared the Bitcoin experiment failed and sold all his coins, citing the governance breakdown directly.

4. Scaling — direct P2P transactions → layer-2 / off-chain

Satoshi wrote (whitepaper § 1, “Introduction”): “…allowing any two willing parties to transact directly with each other…”. The implicit model was that ordinary payments would land on chain.

The reality. Bitcoin’s 1 MB historical block size limit caps the chain at roughly 7 transactions per second (much less under realistic transaction sizes). Routine retail payments cannot fit; even if they could, fees would price them out during peak load. The actual scaling path has been two-layer: SegWit (BIP 141, activated 2017) made room for the Lightning Network, where payments move off chain and only periodic settlements touch the base layer. Custodial exchanges also function as scaling layers — internal transfers between two Coinbase accounts never reach the chain.

The drift began with the block-size discussion in 2010 (Satoshi’s own provisional 1 MB cap, intended as anti-spam) and crystallised through the 2015 – 2017 fork wars. For most everyday use today, Bitcoin functions less like the direct P2P cash the whitepaper invites a reader to imagine and more like a settlement layer beneath several stacked payment systems of varying trust — the outcome James A. Donald anticipated by name in November 2008, when he coined “bink” for a bitcoin bank and cast bitcoins as sitting beneath account money the way gold sat beneath the gold standard.

What this is not

Pointing out drift is not arguing that Bitcoin failed. Some of these drifts are arguably unavoidable consequences of mass adoption: ASIC specialisation is what any economically valuable proof-of-work attracts, custodial exchanges exist because most people do not want the responsibility of key management, layer-2 scaling is the conservative path that preserves base-layer security. The point of this entry is only that any beginner-level description of Bitcoin that omits these four drifts is incomplete — readers will encounter the drifts in practice the moment they actually use a service, and reconciling the gap themselves without a map is harder than acknowledging the gap up front.

The visual glossary describes the protocol’s basic shape as read from the whitepaper and the early design. This entry is its companion: the protocol is real and runs; the operational reality on top of it is also real, and is not the same thing.

This design-vs-current-reality analysis is treated as a load-bearing reference by the bitcoin digital-gold structural-features analysis, which uses this entry as the documented account of the divergence between Satoshi’s protocol design and the operational reality built on top of it.